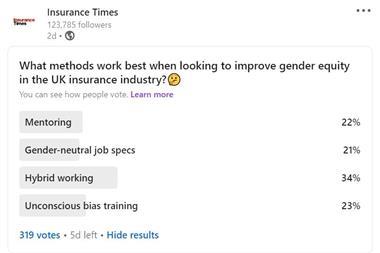

Money and Mental Health Policy Institute has called on the FCA to stop firms from making pricing decisions ‘behind locked doors’

Consumers with mental health issues or neurodivergent conditions are being discriminated against by travel insurers via product pricing and availability.

This is according to new research released by journalist Martin Lewis’ charity the Money and Mental Health Policy Institute, published yesterday (8 February 2023).

A mystery shopping exercise with 15 travel insurance providers conducted in August 2022 revealed that, on average, the price quoted to an individual with stable depression increased by 4% – 53p – compared to someone with no medical conditions.

The average price quoted jumped by 200% for individuals with more severe depression or who were stable bipolar – meaning they were taking medication as required.

The charity’s research additionally found that five out of 15 insurance firms included exclusions for mental health conditions, without reducing the price of the product.

Nine out of 15 firms surveyed also refused to insure a customer with severe bipolar disorder. Five insurers, furthermore, specifically mentioned that consumers waiting for treatment for mental health conditions could not be offered cover.

In some cases, these consumers being on medication or receiving treatment caused travel insurers to view these individuals as higher risk.

For example, the average price increase of a travel policy for someone with stable bipolar was similar to that for someone with more severe depression who had recently been in hospital.

Peace of mind reduction

Considering the findings, Helen Undy, Money and Mental Health Policy Insititute’s chief executive, said: “The insurance industry sells peace of mind, but that’s not on offer for many people with mental health problems, who may arguably need it most.

“It’s hard to believe that these extortionate premiums accurately reflect the risk to insurers, especially when people who have been able to manage their condition for years are still being charged significantly more.”

Money and Mental Health demonstrated that the challenges are not confined to travel insurance, however.

Further surveys of 292 and 211 respondents with mental health conditions, carried out in March and August 2022 respectively, showed that these consumers commonly paid higher premiums across the insurance market generally.

Undy added: “Across many types of insurance, people with mental health problems are facing really poor outcomes.”

One member of the charity’s research community said: “[Being quoted a higher price] made me feel stressed and victimised as I spoke to a few neighbours, [including] one who had made multiple claims, and her premiums were less than half the figures quoted to me.

“I feel that the insurance companies are deliberately overcharging people with mental health [problems] and this makes me less likely to go out, withdrawing from everyday life.”

Call to the FCA

It is legal for insurance firms to discriminate against consumers with mental health conditions when it comes to pricing decisions and products offered, but only if backed by accurate and up-to-date information.

Read: Insurer reacts to rising mental health crisis

Read: Briefing - Insurers are facing a growing confidence crisis

Explore more news content here and discover more diversity and inclusion content here

As a result, Money and Mental Health is “concerned that some firms could be breaking the law”.

The charity has therefore called on the FCA to urgently investigate whether consumers with mental health conditions are being unfairly penalised by insurance providers across the market.

It added that the FCA should also ensure pricing decisions were compliant with legislation, including the Equality Act 2010.

Suggested actions to eradicate the problem include the FCA setting out specific industry expectations around how firms could provide fair value for these consumers, particularly where cover excludes their mental health.

Money and Mental Health also encouraged firms to be more transparent with policy decisions – which must be backed by the latest data and reflect the fact that people can manage and recover from their mental health.

Undy said: “These insurance firms are still making their pricing decisions behind locked doors – in a way that is almost impossible for researchers, consumers or even politicians to hold to account.

“It’s about time that the regulator took decisive action to show that protecting their commercial interests does not put firms above the law.”

A spokesperson for the ABI added: “No one should face a barrier to accessing financial services and our members recognise the importance of being able to offer accessible, affordable cover to as many people as possible.

”Clear communication and transparency around decision-making is crucial, which is why we launched the Mental Health Standards to improve support for people with mental health conditions when applying for travel, health or protection insurance.

”Whilst pricing is a matter for individual firms to decide, the standards include the need for underwriting approaches to be reviewed regularly using up to date data and credible evidence and set out how insurers can explain decisions clearly and provide more options for customers to communicate with them. If anyone is struggling to obtain cover, specialist providers are available to help.”

Hosted by comedian and actor Tom Allen, 34 Gold, 23 Silver and 22 Bronze awards were handed out across an amazing 34 categories recognising brilliance and innovation right across the breadth of UK general insurance.

No comments yet