Market: construction and property

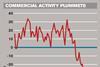

The market is shrinking at a record pace, which will hit insurers' incomes too

You need to register to continue reading the rest of this article and more for free.

(If you’re already registered, please sign in here.)

REGISTER NOW FOR FREE

We’re glad you’ve chosen Insurance Times as your source for industry news and hope you’ve been enjoying reading articles from our award-winning team of journalists.

Gain access to more of our exclusive, breaking stories, interviews and news analysis as it happens. Registering is quick, easy, free, and will also have the additional benefits:

- Uncover Secrets: Dive deep with exclusive annual reports, fueled by expert insights.

- News That Matters: Award-winning coverage & analysis, delivered to your inbox.

- Stay Ahead, Your Way: Daily or weekly - choose your news rhythm.

- Own Your Learning: Curate your knowledge with a personalized library.

Stay on top of the insurance game with our subscription! Get unlimited access to over 80,000 articles, in-depth analysis, exclusive reports by industry experts, and our Five-Star rating system to compare companies and find the best fit for your business needs - view subscription options.