- Home

Opinion: The feedback disconnect – why managers are scared to talk to gen Z

Opinion: The feedback disconnect – why managers are scared to talk to gen Z Insurance Times confirms 2026’s five star insurers for commercial and personal lines

Insurance Times confirms 2026’s five star insurers for commercial and personal lines Eight companies commit to Destination Insurance Charter to become inaugural signatories

Eight companies commit to Destination Insurance Charter to become inaugural signatories Caroline Wagstaff: Forging the LMG into a ‘one trick pony’ for attracting diverse early career talent

Caroline Wagstaff: Forging the LMG into a ‘one trick pony’ for attracting diverse early career talent

- News

- Analysis

- Destination Insurance

- Brokers

- Insurers

- Ratings

- Research

- Fraud Charter

- Topics

- Events

- Expert Views

- Edition

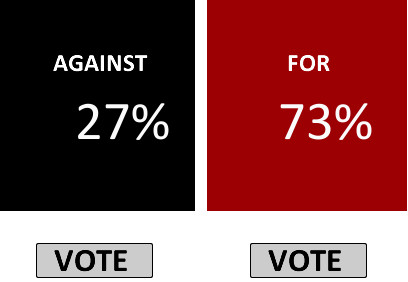

Our online vote is now closed. Thank you to everyone that voted and commented. You can still view the debate video and read the viewers comments below.

The Debate

Video:

Insurance Times Debates - Compenstation Culture

Moderators View

Is there a compensation culture? It’s a debate that has been rumbling on for years, but has increasingly gained importance as personal injury and payment protection insurance claims have exploded in recent years. Personal injury lawyers claim it it’s a myth, and insurers are said to blame the compensation culture to cover up for higher premiums. The insurance industry fiercely contests there is a compensation culture, especially in personal injury, which has been fuelled by the aggressive practices of claims management companies and lawyers’ eagerness to make a quick buck. In the Insurance Times Online Debate, “Is there a compensation culture?”, Claims Standards policy director Andy Wigmore and AXA Underwriting Managing Director David Williams go head-to-head to tackle this debate. Wigmore, known for his polished performances as a debater, argues there isn’t a compensation culture, while, Williams, one of AXA’s most outspoken and charismatic directors, goes on the offensive and debates that there is not only a compensation culture, but that it is also seemingly out of control. You the viewer will decide the winner by watching the debate and then clicking on who you think has won the argument. The full results will be published here on the website and in the magazine on August 16. Keep your eyes peeled. It’s going to be interesting.

Is there a compensation culture? It’s a debate that has been rumbling on for years, but has increasingly gained importance as personal injury and payment protection insurance claims have exploded in recent years. Personal injury lawyers claim it it’s a myth, and insurers are said to blame the compensation culture to cover up for higher premiums. The insurance industry fiercely contests there is a compensation culture, especially in personal injury, which has been fuelled by the aggressive practices of claims management companies and lawyers’ eagerness to make a quick buck. In the Insurance Times Online Debate, “Is there a compensation culture?”, Claims Standards policy director Andy Wigmore and AXA Underwriting Managing Director David Williams go head-to-head to tackle this debate. Wigmore, known for his polished performances as a debater, argues there isn’t a compensation culture, while, Williams, one of AXA’s most outspoken and charismatic directors, goes on the offensive and debates that there is not only a compensation culture, but that it is also seemingly out of control. You the viewer will decide the winner by watching the debate and then clicking on who you think has won the argument. The full results will be published here on the website and in the magazine on August 16. Keep your eyes peeled. It’s going to be interesting.

Argument Against

Andy Wigmore

Policy Director, Claims Standards Council

- (1) Does the UK have a compensation culture?

(00:00:10:08) - (2) How would you describe the current system for personal injury compensation in relation to whiplash?

(00:01:35:09) - (3) What do the public think?

(00:04:17:07) - (4) Do so-called claims farmers help consumers?

(00:06:15:15) - (5) What are the solutions?

(00:08:00:28) - (6) Are the government and associated industries successfully on track to deliver the solutions?

(00:10:18:07)

(1) Does the UK have a compensation culture?

Claims Standards Council policy director Andrew Wigmore rejected the idea of a compensation culture.

He said: “If you take a look at the actual figures of those accidents that occur in this country you could argue that they have been paying pretty much static over the last five six years and they have been slight rises, but nothing that would actually demonstrate that there is a compensation culture.”

Wigmore added that the term ‘compensation culture’ had been hijacked by the media and others.

He said: “As a consequence of that, the label ‘compensation culture’ I think has been misused dramatically.”

He argued that the way the media have bandied about the phrase could also have led to the perception that such a culture really existed.

(2) How would you describe the current system for personal injury compensation in relation to whiplash?

Wigmore said that many canny consumers had taught themselves how to successfully make whiplash claims by looking on the internet.

However, this only came from a “very tiny” section of the public, he added.

He said: “The trouble is, the diagnosis process I don’t think has kept up to speed with the way current injuries are actually measured at the moment.

“Currently you have to have a medical report, which is absolutely right. But doctors at the moment use quite an old system in determining the diagnoses of whiplash.”

Wigmore said that if this diagnosis process was brought up to date, then this would remove a large chunk of spurious whiplash claims.

(3) What do the public think?

Wigmore said that the public now know so much about how to make a claim that many choose to submit fake ones, and that the recession had amplified this.

He said: “In the current climate, if you think about it, people are struggling.”

The public were also being enticed to make claims by all players in the insurance industry, including claims management companies (CMCs), lawyers, insurers and brokers, he added.

He said: “So, this perhaps is where the perception of a compensation culture comes from, because of the way, and the aggressive way, people market to acquire a customer.”

(4) Do so-called claims farmers help consumers?

Wigmore said that the term ‘claims farmer’ had been mis- used, and that it should apply to the whole insurance industry rather than just CMCs.

This included lawyers, insurers and brokers, he said.

He added : “Everyone’s at it. I have to say, the claims management companies, the purist ones, aren’t very good at it anymore. In fact, the insurers and the lawyers are much better, and they spend a whole lot more money on trying to advertise those services than claims management companies ever did or ever could.”

(5) What are the solutions?

Wigmore said the solutions lie in separating the claims from car crashes from claims for employers’ and public liability.

He said that insurers and brokers would end up dominating the former, and that those claims would become increasingly commoditised.

“I think what will happen is you will see the lawyers dealing with the employment liability and public liability, you are going to see a separation,” he said.

“You’re starting to see it now, where a lot of the alternative business structure (ABS) processes that are being proposed, they very much look at the commoditisation of a road traffic accident.”

He concluded that this separation would lead to the personal injury claims process becoming smoother and more efficient as insurers can bring their operational efficiencies to bear.

(6) Are the government and associated industries successfully on track to deliver the solutions?

Wigmore said that Solicitors’ Regulation Authority rules on allowing ABS’s was good news for the insurance industry, but that government banning of referral fees was “a red herring.”

This was because referral fees could continue in another guise after the ban, he explained.

He said: “The determination of a referral fee is a difficult one. What is someone else’s referral fee is someone else’s commission, which is someone else’s provision of service.”

Andy Wigmore

Policy Director, Claims Standards Council

Andy’s professional background is in public relations and healthcare, and, with Health-Media.co.uk was one of the pioneers of internet health news services. Andy was the driving force behind the establishment in 2004 of a self-regulatory body for the claims management sector, and when the role was taken on by the Department for Constitutional Affairs (now the Ministry of Justice) Andy was asked to convert the CSC into a trade body and lead it.

He is managing director of the Wigmore Media Group, whose PR and marketing clients include some of the biggest names in the UK health and legal sectors.

At present Andy is also the London representative of Team Belize, the Belizean national participants in the London Olympic Games.

Argument For

David Williams

Managing Director of Underwriting, AXA Insurance

- (1) Does the UK have a compensation culture?

(00:00:54:21) - (2) How would you describe the current system for personal injury compensation in relation to whiplash?

(00:03:33:03) - (3) What do the public think?

(00:05:31:20) - (4) Do so-called claims farmers help consumers?

(00:07:14:09) - (5) What are the solutions?

(00:09:21:06) - (6) Are the government and associated industries successfully on track to deliver the solutions?

(00:12:04:21)

(1) Does the UK have a compensation culture?

AXA Underwriting managing director David Williams said that a compensation culture definitely existed in the UK.

He said: “I think anybody who says that we don’t have a compensation culture problem is just blind. They are kidding themselves.”

Williams added that insurers handled around 570,000 whiplash claims a year, at a rate of one per minute on average.

He added: “I speak to my colleagues across Europe and they joke about it, they say we got the weakest necks – no, we don’t have the weakest necks.

“What we have is a compensation culture, represented by those whiplash numbers, but fuelled by the access to justice bill and claims farming, which is getting worse and worse.”

(2) How would you describe the current system for personal injury compensation in relation to whiplash?

Williams said that the current whiplash claims process was more suited to making money for third parties than compensating the genuine victims.

He added: “We have a process where serious inured people are auctioned off on websites, we have a legal system where fees are so high that 75% of them can go out in terms of referral fees.

“This contributes to a situation where, as I say, the injured party is probably the last person that people are really thinking about, other than that they represent an opportunity to earn money .”

(3) What do the public think?

However, Williams said he thought the public were shocked at the way they were encouraged to make claims.

He said: “I think there was an ABI survey that asked people how they felt about being texted, emailed and cold called, and 92% of them were absolutely appalled with this.”

Williams added that he was surprised to hear that three out of four people had received an

unsolicited text or email, and dubbed these marketing tactics as “hassle.”

“You get these texts that if you have not had a claim, you get somebody trying to persuade you to make a claim because they can earn from it,” he said.

(4) Do so-called claims farmers help consumers?

Williams’s view was that claims farmers add no value to consumers, and that defence that these companies give access to justice was weak.

He said: “I think there are many ways, particularly in this digital age, of making people aware of their rights and the ability to make a claim to compensation.

“All claims farmers do is add an additional layer to the process and an additional cost.”

He said these companies encourage spurious claims, especially in motor, but increasingly in employers’ and public liability as well. Williams attributed this to the incoming legal aid, sentencing and punishment of offenders act that will shake up the claims management sector.

(5) What are the solutions?

Williams said that the solutions included the Jackson reforms and the legal aid act, and added that he wanted to see these fully rolled out.

He said: “We need a better solution for diagnoses of whiplash, so that if somebody really is suffering then they get appropriate training rather than - as I say - just an opportunity to earn.”

Reducing legal fees for whiplash cases will also lower the volume of claims, he said.

“How about increasing the small claims limit on injuries claims to £5,000?” Williams added. “That would single-handedly take out the opportunity for people to earn money unnecessarily, and I think would correct things.”

(6) Are the government and associated industries successfully on track to deliver the solutions?

Williams said that government was definitely on track to deliver the solutions, and that Labour was also very supportive.

He said that Jack Straw’s campaign for whiplash reform has been vital in publicising the issue, but that the claims arena generally needed legislation that was strictly policed.

Williams added: “So for instance, everybody knows about the problems with cold calling generally, and everybody knows these things are being enforced.

“We need to see some real action, and the end product, I suppose, but certainly I am quite positive about where things are heading.”

David Williams

Managing Director of Underwriting, AXA Insurance

David has over 20 Years experience in general insurance, roles including chief commercial underwriter at one of AXA’s largest branches, reinsurance manager and casualty insurance manager, before moving to claims in 2003. After leading AXA’s Personal & Commercial claims teams for 8 years, the split of AXA Insurance saw David return to underwriting as claims & underwriting director for the newly formed Commercial Organisation.

He was heavily involved in the government and ABI responses to the ‘liability crisis’ from his time as casualty manager, and continues his lobbying work as the insurance industry looks to remove unnecessary costs and delay from the current adversarial compensation process. He is an outspoken critic of referral fees, credit hire, high legal costs and the escalating issue with whiplash claims.

As well as operating at an executive level within AXA Insurance, David is a non-executive director of AXA Assistance UK and chair of the CII Underwriting Faculty. He was previously a board member of the CII / CILA Faculty of Claims, a member of the National Stakeholder Council for the government’s Workplace Health Connect initiative, and was a director of Thatcham, the insurance industry motor vehicle research institute for four years.

He is a member of the AXA Group P&C and Claims boards and has represented the UK on asbestos, health, pollution and fraud issues. He speaks regularly at conferences and other events in the UK and Europe on a variety of subjects including most recently motor claims costs, improving customer satisfaction, flooding and climate change

David has also appeared on BBC Breakfast TV, Sky, Channel 4 and BBC News, as well as Radio 4’s Today Programme, being interviewed on topics varying from compensation culture to business crime.

David originally hails from Bristol (explaining his passion for Bristol Rovers!) but now lives in Suffolk with his wife Catherine and two young sons Evan (6) & Ryan (4).

Views from the Audience

Thank you to everyone who commented on our debate.

Michael Hardacre, Partner, Pannone Affinity Solutions

“I do claimant and defendant work, so I see both sides. I am forever at a loss to understand how we have reached this stage where everyone is shouting and screaming at each other and there is precious little common ground. From a Claimant perspective, it’s whiplash RTA’s that have caused the problem. They are the example that are cited time and time again of people “trying it on” but ultimately, with an injury for which there is no objective diagnostic criteria, this was bound to happen. There will always be some people who think they can beat the system. It might be unfashionable to say it, but I don’t think for a minute that it’s more than a tiny minority who actively try to do so. I think most people are just sucked into the claim from the moment they ring their insurer to report the accident or go into a garage to get their vehicle repaired or whatever and then everyone pounces on them. They get onto the conveyor belt and they don’t know what on earth is going on because they’ve never been through this before. Are they exaggerating or making up their injury, of course they aren’t. They’ve got a short acute phase of injury, followed by niggles for a few months and then they’re fine. The vast majority of whiplash RTA’s are settled quickly and proportionately in terms of costs thanks to the portal. All parties, CMC’s, claimant solicitors, defendant insurers have to accept that capture of new claims has gone bonkers in the last few years. There is no doubt that this is due to referral fees and there being a “value” to the claim itself, but banning referral fees won’t change that, if insurers and CMC’s simply set up ABS’s to park all the claims in after April 2013. And I think it’s disingenuous to the point of shameful for insurers to pretend they aren’t complicit in this with either third party capture schemes or using referral fees as a significant income stream. From a defendant point of view, my clients are self insured companies who generally have a pretty robust approach to claims because it’s their own money on the line. What I find frustrating is if insurance companies were similarly robust they might find themselves winning a few more cases at trial, because there has been a sea change in the approach of the judiciary in the last few years. If you ask Zurich, who insure many councils, I would be amazed if did not confirm that is the case. They routinely defend cases to trial. They will only admit breach where they haven’t got a leg to stand on and long may that continue. If claimants think they can chance their arm and get away with a fraudulent claim it can only possibly be because they think they can get away with it and the only way they can get away with it is if defendants and insurers are daft enough to pay them off without properly investigating their claims.”

Alex Fitzpatrick, Insurance Analyst, Datamonitor

“Increasing claims and costs per crash, whiplash occurring after impacts below(!)walking speed - definitely a compensation culture. It will continue as people look for blame in everyday life, especially as incomes remain low. Only a ‘man-up’ attitude will change things - legislation would only slow but not stop the trend.”

N Gittins, Senior Litigation Executive, Curtis Law Solicitors

“The so called compensation culture does not exist. What does exist is an environment where insurance companies, with their vast resources built on ever-increasing premium prices, are able to lobby politicians and media outlets to create this mirage of a compensation culture so that the public are led to believe that their increased premium prices are as a result of rampant legal costs, bandit-like lawyers and greedy Claimants. The whole suggestion of a compensation culture is merely a smokescreen and a convenient scapegoat when it comes to increasing premium prices. A factor which contributes substantially to high premium prices, but will never make the press, is the poor decision making and unnecessary penny pinching which occurs within insurers’ offices when it comes to genuine claims. Decisions made to try and save £100 here £300 there, which ends up costing 10 times that amounting costs when Court proceedings become necessary. Finally, let us not forget that the very insurance companies who bemoan this so called “culture” are guilty of selling their own policyholder’s details to solicitors following an accident and they also enjoy financial benefits arising from provision of various services following such accidents. You cannot call yourself a victim when you have helped to stoke the fire.”

Victoria Elliott, Paralegal, Berrymans Lace Mawer Solicitors

“Agree with the motion set out by Axa’s David Williams, there is a compensation culture”

Andrew Hooper, Director, Acxiom Ltd

“I do not agree that there is a compensation culture”

Anon

“I do not feel that it is right, but there is definitely a creeping insurance culture in the UK, with more and more people following the new adage “where there’s a blame there’s a claim”. It is seen as a quick buck, as well as a way of shifting the responsibility for your own actions onto a third party.”

Anon

“Any perceived increase in claims is largely driven by the rise of the Claims Management Companies and very often their aggressive marketing. Sadly solicitors are being painted with the same brush. Why CMC’s were ever allowed to exist is just beyond me.”

Anon

“Yes we do have a specific problem with the so called claims farmers instigating whiplash claims but generally our ‘nanny state’ has stopped people from thinking for themselves and being responsible for their own safety. Many people believe that responsibility lies with everyone other than themselves and when things go wrong they want to blame & claim for anyone & everyone instead of realising that they need to take on some accountability for themselves.”

Anon

“Isn’t it an obvious answer? This has been going on for years now, and accompanies and sits side by side the mess that is the culture created by the benefits system so poorly managed by the last Government. It is high time legislation was introduced to curb it, a difficult thing to do without affecting those who have suffered a genuine loss and who are entitled to some form of reasonable compensation. When I was a young adult some 30 years ago, a person in the legal profession was someone to look up to and respect as a pillar of society; oh how things have changed!”

Pauline

“There may be a small amount of dodgy people out there that abuse systems, but that stems to all different systems too not just claiming for compensation such as claiming for housing etc…there are a multitude of people falsely claiming for benefits and that money comes out of our pocket however the bad press is seems to concentrate on this so called Compensation Culture stating that the premium rises are down to that but I have to disagree based on my own experiences with my insurance company slowing the whole claim process down in order to build their costs…the premium rises are of real benefit to the insurance companies and they should be penalised for their faults, I recently used a claims company for my vehicle claim and they were fantastic, I had no delays it was seamless… as it turned out a cheaper outcome for the other side than going through my insurance company. Surely there are ways of battling with the fraudulent people staging accidents, maybe in the punishments were more severe people would think twice about making a false claim? People like me need to be able to claim, if I can’t work due to an accident then I can’t pay my mortgage etc…is anyone considering the genuine people that have accidents when they are assessing the so called Compensation Culture and does compensation stretch to claiming for benefits too?”

Anon

“If a person has had a genuine accident, they should have the right to bring a claim for compensation otherwise industries etc would fail to follow health and safety and welfare of others. Motor Insurance is in place not just for the benefit of compensation but to alert the driver of their responsibilities and to adhere with the highway code. There are ways to ensure claims are legitimate and by no means am I supporting a culture for fraudulent claims however with the correct processes in place, people should be allowed access to justice.”

RR, Axa

“If someone is injured and put out of pocket they have to get put back into the same position in a way that is easy and convenient for them, and they need to be represented by someone who is specialised and is on their side, not just cost effective for the insurance industries profit margin. If you don’t like CMC’s don’t use one, but other people clearly do, and they use them in large numbers… why? BECAUSE THEY WANT TO.”

Disgusted

“Ummm, but this is on the insurance Times website! This is another prime example of a money hungry industry using dirty tactics to influence politicians to change the law so they can improve profits at the expense of injury victims. Perhaps if you want to reduce premiums you should spend a few million less on TV advertising rather than trying to reduce the rights of needy injury victims.”

Kathy Richards, DLG

“I disagree with the motion, there is not a compensation culture”

Anon

“It is the insurers who are driving up the premiums. In order to get on the side of an insurer listening government, the insurers have suddenly substantively increased the premiums. How conveniently timed.”

Richard, Armstrong; Company, Wheelers LLP

“Insurers harp on about the evils of referral fees yet it was the insurers who introduced them. They created their own panel of firms and used their first point of access position to hoover up hundreds of thousands of cases. They effectively sold those cases to their panel firm whilst at the same time taking money from their policy holders for what were in reality bogus Legal Expense Insurance Policies. Firms who were not on the restricted panel could not compete and were forced into using Clams Management Companies, to whom they obviously had to pay a fee. As the panel firms became more dependent on the bulk work providing insurer, so the insurers hiked up the fees. At all times the solicitors were the ones being squeezed. Now, through recent changes in the law, insurers see the opportunity to own their own firms and cut out the competition, so they suddenly decide referral fees should be banned. As for increasing the small claims limit, from fact I know of several cases where insurers have made a first early offer on a case of £2750 or less, but that case has in fact gone on to be determined to be worth in excess of £45 000, and on some occasions hundreds of thousands of pounds. Insurers make profits by receiving premiums and not paying out on claims. If Joe Public cannot recover legal fees he won’t use a lawyer. If he does not use a lawyer you can be certain insurers will not pay what they should, when they should, and it is Joe Public on the street who will lose out.”

Anon

“The compensation culture does appear to be limited to a specific type of accident, namely road traffic accidents. The so-called culture has been fueled by the media, claims management companies and insurers alike. Fraud must be tackled head on and insurers are certainly not helping the situation when they make pre-medical offers to settle. I am sure we would see a reduction in fraudulent claims if insurers were willing to share information about their concerns with solicitors who at the end of the day are acting on the instructions of their client. On the flip side, I believe a large proportion of genuine claimants are not making claims for compensation where they have been injured in all types of accident as a result of someone else’s negligence because they do not wish to be branded as a compensation culture statistic.”

Anon

“Any perceived increase in claims is largely driven by the rise of the Claims Management Companies and very often their aggressive marketing. Sadly solicitors are being painted with the same brush. Why CMC’s were ever allowed to exist is just beyond me.”

Lee Jones

“The reason for the rise in Motor injury claims is from the change of stance of insurers, who have increasingly become involved in injury claims capture and referred the injured parties to their panel firms. Or the insurers making direct contact with third parties and settling claims directly. Not only that, but where does all the data come from that these pests sending unsolicited text messages to people use? Yes you guessed it, the insurers! They appear to be the authors of their own misfortune. According to all the headlines of late, most insurers seem to be bouncing well back into profits and COR’s are well below 100% again. Is this due to the savings they have made from the fixed costs regime of the MOJ process? In my opinion, the changes which have been rushed through parliament have been premature and simply bankrolled by the insurance industry, who continue to be poorly managed and seek to blame an industry for their own failings, rather than rectify the problems on their own doorstep”

John Cassidy, Director, Clement Gallagher & Co Ltd

“I agree with David Williams, there is a compensation culture”

Anon

“There is a compensation culture. It is fuelled by no win no fee solicitors, insurers selling details of those in accidents to such solicitors and also insurers unwillingness to fight spurious claims in court as it is cheaper to settle them out of court. It is easy to get a large payment for the merest vehicle collision where very little injury is sustained. I know someone who had a very low speed car accident where she was hit in the rear and within a day she was being called by unsolicited accident claims companies and, despite suffering the slightest ‘whiplash’ injury, i.e. a slightly stiff neck’, received over £1,900 in compensation. Insurers are encouraging this behaviour and Joe Public is paying for it. What a surprise the industry has a bad name.”

A senior commercial broker

“As an insurance broker and also a whiplash sufferer (10 year and 6 days), I do know from experience the results of a none fault motor accident. I had to go through several interviews and at least three medical examinations whilst making a claim to cover medical costs and a small amount of future physio costs (which run out within the first year of settlement). I do believe that this no win no fee culture damages both the Insurers and the people who do truly have an injury which is labelled as “whip lash”. In this current climate, nothing is deemed to be blame free, so a lot of time and money is wasted on fraudulent claims and time wasters. ”

David Pipkin, Director, Temple Legal Protection |Limited

“There is too much propaganda. We need to look at objective evidence which suggests there is not a compensation culture. What we do have are certain organisations preying on a vulnerable part of society to encourage claims to be made. These organisations include the very same companies who provide liability insurance. I submit many thousands of worthy victims of negligence do not currently claim and form April next year many more will be unable to do so.”

James Willis

“Insurers contribute to the compensation culture to the extent that they provide ATE insurance to fund no win no fee cases through personal injury solicitors”

Anon

“Constant fraudulent claims being presented when there are no witnesses to an accident.”

Adrian Wynne, Partner, BTW Solicitors

“Extremely insulting to describe matters as an “opportunity to earn”. Nothing other than a smear campaign to frighten genuine claimants from access to justice.”

ANON

“Yes I believe we are in a compensation culture, it’s an opportunity for some to earn quick money. We live in a culture of blame, where some people believe it is their right to claim for another person’s ‘negligence’. I have heard some people even refer to it as ‘the insurer’ asks for it; with increasing fees and complicated wordings, making a claim is a hefty challenge. Insurers are not transparent and quick to make excuses for increasing premiums for the majority generalising potential high risk.”

Paul Davey, Senior Manager, Hays

“There is a growing acceptance in British culture of ‘why shouldn’t I claim my share’ whether its exaggerated or false whip lash claims or the PPI grab that’s taking place, all of which erodes confidence in the correct compensation systems and processes. Clear advertising and canvassing / cold calling regulations need to be put in place, if nothing else to stop me getting pestered three times a day by PPI claims companies!”

Richard Mikula, Director, Topaz Insurance Ltd

“There is only a compensation culture because insurers have allowed it, and encouraged it to strive. The fact is Insurers have seen this coming for years, but did nothing. Rather than stamp out bogus claims they paid them. It’s all a question of the balance sheet. The more rates go up the more claims will be made.”

Jackie Hagen, Commercial Lines Executive, Lloyd Latchford Insurance Consultants Ltd

“Aside from the increase in the number of personal injury claims coming in, the circumstances around them is getting more obscure. When the opportunity for a payout comes along, people are no longer willing to take responsibility for their own actions.”

Anon

“I’m not sure that “culture” is the right word as that suggests a widespread acceptance that getting compensation is a right following any incident. In reality there are a number of rogue companies exploiting loopholes that the industry has been using for some time to get downstream income as Underwriting profits and commission are squeezed, and at a company level there has become a feeling that because some people are doing it, if you don’t you are losing out. I suspect the public, by and large, hate the cold calling, bombardment by various companies following an accident and the assumption they will want something for nothing. There is no silver bullet solution - banning referral fees can’t hurt and improving diagnosis of whiplash will move things forward but we need all insurers and brokers to start working together to reduce the cost of claims across the board and remove the financial incentives that have driven this whole issue.”

John Cassidy, Director, Clement Gallagher & Co Ltd

“I agree with the motion – there is a compensation culture”

Anon

“There is a compensation culture. It is fuelled by no win no fee solicitors, insurers selling details of those in accidents to such solicitors and also insurers unwillingness to fight spurious claims in court as it is cheaper to settle them out of court. It is easy to get a large payment for the merest vehicle collision where very little injury is sustained. I know someone who had a very low speed car accident where she was hit in the rear and within a day she was being called by unsolicited accident claims companies and, despite suffering the slightest ‘whiplash’ injury, i.e. a slightly stiff neck’, received over £1,900 in compensation. Insurers are encouraging this behaviour and Joe Public is paying for it. What a surprise the industry has a bad name.”

Adam Hughes, BDM, Maps Legal Assistance

“I do not agree that there is a compensation culture”

Chris Bancroft, Account Handler, McClarrons Ltd

“I agree that there is a compensation culture”

Stephen Fisher, Chair, RSI Action

“Agree with Andy Wigmore, there is not a compensation culture”

Bob McMahon, Commercial Account Executive, The Thomas Gray Partnership Ltd

“Agrees with Axa’s David Williams, that there is in his opinion a compensation culture”

Elaine Mason, Managing Director, Belvedere Mead Ltd.

“As I vote I wonder whether the results would be different if the audience of the debate was note those working in the insurance profession but were for example a cross section of the public at large. The fact that Andy highlights that accident numbers over recent years but fails to mention that the claims count have dramatically increased would highlight that people do think of claiming more often than not. With all the advertising and the good and bad of the claims management companies then how can individuals not be thinking about a claim. However, I think the BLAME culture exists across a lot of Society these days. Something happens and it must be somebody’s fault perhaps the breakdown of our social fabric is also partly a contributor but that is an entirely different debate!”

Wayne Calderbank

“We live in a blame culture society fuelled by various sectors which make huge profits on the back of genuine and disingenuous claims. This has created a Compensation Culture. ‘Where there is blame, there is a claim’ has been replaced with ‘where there is opportunity, it can be exploited’. Radio advertisements offering upfront payments to potential claimant’s and suggestions that you are suing your employers insurers, not your employer’s (factually incorrect) entice those in financial hardship to add to the problematic situation.”

Ant Gould, director of faculties, CII

“I have voted that there isn’t a compensation culture but this is only in respect of the term culture. There are undoubtedly more people encouraging others to make a claim - including claims management companies. However, when it comes to the question of is there a natural propensity to make a claim, i.e., an underlying view by society that everything is always somebody elses fault and nothing is an accident - then I don’t think we are there yet. I may be being naive but I still think the vast majority of Joe and Jane public are a long way off from being knee-jerk claimants (for want of a better word).”

Anon

“Andy’s argument seems to focus more on whether all accident management companies are the same rather than whether a compensation culture exists. I’m sure some of these companies are more honest than others but that doesn’t change the fact that the UK has a disproportionately high percentage of small injury claims when compared to other similar developed countries. Also, Andy seemed keen to wrap up the debate towards the end. Did he hear an ambulance drive past?”

Toby Lerone, Researcher, Hershey

“Having recently had an accident, involving me careering from the road into a tree, I had suffered injuries. There were claims managment people on hand at the hospital willing to pursue a claim against the land owner for my injuries. However many times I tried to advise the persons concerned that it was I who had caused the accident, they were insistent I could make a claim for a “few thousand quid”. Dreadful!”

Martin Ashfield, Axa Commercials

“Whether we judge it from relentless TV advertising, figures showing PI claims per vehicle or numerous contacts to get you to make a claim, it seems abundantly clear that regrettably we have descended into a compensation culture.”

Simon Bennett, CAA

“Why would anyone think there isn’t a compensation culture? Dealing with thousands of claims every week I know there is a compensation culture aided by ruthless TV advertising, Newspapers, spam emails and text messages. But this aside tackling the route problem would be a more pragmatic approach to why. I do agree with Matt (below) that the likes of Jack Straw should tackle the deep rooted problem of cash for crash, fraud and unsolicited text messaging before blaming Insurers, brokers and claims management companies.”

Anon

“A 30% increase in new claims receipts year on year over the last 3 years, on a closed book of EL business tells me that there is. That, coupled with daily unsolicited text messages advising me to make a claim myself. I’m so tempted to call the number just to see what happens!”

Anon

“It is too easy for claimants to start an action and for solicitors to make money at the expense of claimants and ultimately the insuring population because it impacts across all sectors of society and business.”

Anon

“There’s only compensation culture in personal injury - where it’s an utter vulture fest! Other places its fine. You guys need to see the bigger picture.”

Emma Claxton, Axa Insurance

“There is definitely a compensation culture. Customers need lots of guidance and hand holding when they have suffered a genuine injury. The fact that some of the companies that offer to deal with their claims often only see them as a money making opportunity is shocking.”

Stephan Dequaire

“Should this topic really be up for debate?”

Anon

“Whilst I certainly agree that there is the perception of a compensation culture, the evidence being the increase in the number of claims in recent years, the VAST majority of insurers have helped drive that increase by actively encouraging their own policy holders involved in “non-fault” accidents to make a claim so they can enjoy the “income stream”. Let’s look to improve the system but for god sake let’s stop with the “we (the Insurers) are the innocent victims of the actions of others” bleating. It’s disingenuous and the Industry, if it hasn’t already done so, will lose credibility as the public realises who is (at least in part) responsible.”

Neil Daniel, Head of counter fraud and investigations, Gab Robins

“If you dealt with as many false claims as I see, and saw the reactions and heard some of the stories I have heard, there would be no doubt in your mind either. What topped it for me however, is that 6 months ago whilst out with my family I saw a car bump the rear of another both in front of me. Low velocity impact personified. As we were in a queue I got out and helped the drivers with what to do. Recently I received a call at home from a solicitor asking for my support in a PI claim. I explained my role as a fraud manager and the solicitor hung up.”

Liz Smith, Franchisee, Coversure Insurance Services in Middlesbrough

“As a broker we have seen a marked increase in compensation claims. The insurance companies should do away with third party and third party fire and theft covers. If there was only comprehensive cover any claims would be dealt with immediately by the clients own insurance company which in turn would help rid us of the Accident Management companies whose main source of income is on the credit hire. These companies should also be regulated as we are.”

Anon

“Without a shadow of doubt there is a compensation culture. Working in claims for 22 years, I have seen this first hand.”

JEREMY SMITH; Job Title = SENIOR CLIENT EXECUTIVE; Company = MARSH

“Agree there is a compensation culture.”

Anon

“RBS have announced today they are setting aside £125m to pay compensation to customers affected by its recent IT systems failure. Will the press become excited that IT is contributing to the compensation culture?”

Anon

“Absolutely yes, there is. Thirty years ago my boss at the time said that a few years down the line we would be ” just like America “. How right he was. I see it day in and day out.”

Anon

“There is no doubt that a culture exists, there is such a thing as an accident and sometimes nobody is to blame or the individual themselves has put themselves at risk but the culture now is, I am injured someone must pay.”

Matt

“Interesting that Jackson and Straw et al focus on blaming claims management companies and medical agencies rather than tackle the deep rooted problem of cash for crash, fraud and unsolicited text messaging”

Anon

“There is most definitely a compensation culture in the UK. It is being driven by claims farmers who constantly bombard individuals with phone calls and texts promising thousands of pounds in compensation for injuries or mis-sold PPI to people who have never suffered an injury or taken a loan. These companies and the sources of their information need to be properly regulated.”

Anon

“There is a steady progression of Insured’s claiming for losses that once upon a time would have been put down to life experiences. We are becoming the United States of Britain.”

Stuart Cliffe, COO, NABIC

“Claims companies, intermediaries, insurers, solicitors, doctors, hire companies and repair centres have all contributed to and encouraged the “culture”. Policyholders are more likely to find that a claim is prewritten and thrust in their hand, than have to demand access to their advisors so they can pursue a claim of their own choice. This is a Financial Services market problem, not a social one.”

Anon

“With the future reforms I am inclined to think this will only increase the number of claims pursued particularly for eg stress……”

Tony Prior, Director Asset & Risk Appraisal, American Appraisal UK Ltd.

“I believe this partly springs from the US Culture that has been with us for a number of years and the growing number of people in the UK who are always looking for “something for nothing” and the PC Culture, that says everything is someone’s fault.”

Mr N Slack, Commercial Manager, Bale Insurance

“I agree with David Williams that there is a compensation culture”

Anon

“Of course there is a compensation culture. This isn’t just insurance related either. One only has to look at the sheer amount of benefits being frittered away on individuals with no real entitlement to them to recognise that. Regarding the 2 comments (one from Victoria and one from Anon) in respect of Insurers “profiteering” from the ‘ghastly’ motor Insurance premiums perhaps they could advise the rest of us which Insurers over the last 5 years have actually returned a Motor Underwriting profit in isolation. I would be keen to hear from them.”

Steve Gelder, Managing Director, Gelder Group

“No win no fee solicitors should be castrated & then publicly flogged [maybe I am a bit to right wing!], they are killing business and the Government needs to step in.”

Lee Stratford, Administration Manager, Insurance 4U Services

“It’s about time all these TV adverts were stopped, txt messages as well along with tonnes of post and emails stating you could be entitled to thousands in compensation.”

Anon

“We are not known as the whiplash capital for nothing! Culture is not however limited to motor where aggressive marketing by AMC’s has fuelled the public’s perception that they can claim however they are injured, even when a most trivial injury occurs.”

Kerry Bluett, Divisional Director, Bluefin

“As a broker we see so many conflicting claims, those reported by our client against those reported by third parties. No vehicle damage and yet we see claims for many thousands of pounds for injury, what injury!! It does make my blood boil especially ambulance chasers who are nothing short of parasites.”

Gavin Fisher, Partner, Townsend

“It is self evident that this exists and most claims are frivolous and verging on fraudulent. These are pushed by solicitors and unregulated claims management(reg by the MOJ is not regulation) firms. Little is done by the insurers to fight these. Legal aid should be withheld for these types of claims. They are not in the public interest”

Victoria

“Why not pose the question - “Is there a Compensation Culture?” rather than make a positive assertion that there is and then ask people to agree? Rights awareness is not compensation culture. If you are ever involved in an accident and need assistance with your injury claim where would you turn? The right of redress has been part of the Common Law since the Middle Ages. With an expanding population there are an increased number of torts. Insurance companies profit from the legal requirement to have insurance in place since 1969 for Employers Liability and 1930 for Road Traffic Accidents. Has anyone got a view on need to grow profit at the expense of victims of negligence?”

Anon

“The amount of shameless advertising on TV and in Newspapers has led to a compensation culture. This is then not helped by the excessive costs claimed by Claimant firms who try to inflate claims to increase their own fees.”

Anon

“The Better Regulation Taskforce found only that there was a perceived compensation culture and not an actual one! Don’t fuel further misconception!!”

Andrew Greenhalgh

“Having recently been involved in a fairly minor motorcycle accident, I’m appalled by the number of people who think they can ‘earn’ something from the insurance companies. What should have been a £5k claim for two written off low value vehicles now has at least £5k worth of solicitors fees, hire vehicle charges and storage charges alone after only 4 weeks. I’ve found it incredibly difficult to give the hire vehicle back, the hire company just don’t want it back, they’d rather it was out on hire earning them money. The third party involved clearly wasn’t injured, I wasn’t really injured after hitting a car on my motorcycle at circa 30mph so how the driver of the car was injured I have no idea. Clearly the third party driver has put an injury claim in on the advice of his solicitors. As the accident is likely to be split liability why can’t the two insurance companies just speak to each other right from the very beginning, agree the damage and injury costs and split the bill. It should be so simple. As soon as someone thinks they can charge for something that the insurance companies will just fork out for they will do it. Insurance companies need to take control and work together.”

Anon

“Is it not the fundamental principal of insurance to provide compensation in the event of a loss? Therefore the more insurance sold, the more claims or compensation provided. Who is doing the best out of this culture? One only has to look at the profits of insurers to see why a ‘compensation culture’ or should we call that ‘insurance culture’ has been brought about!”

Anon

“The real culture is that of insurers trying to dodge paying out for what they should. You only have to look at the disgraceful actions of those insurers trying to dodge paying out for asbestos disease to get a reality check on this nonsense.”

Anon

“Clearly we have a compensation culture, otherwise as a nation we would not readily make compensation claims to the increasing numbers that currently exist. The question that we should be asking ourselves is whether we believe a significant number of those claims made are either outright false or otherwise exaggerated out of proportion to the initial injury suffered. The problem for the industry is that we have Solicitors and Claims Management Companies who use constant and aggressive marketing campaigns encouraging people to make a claim (where there’s blame theirs a claim). Then we have medical experts who would no doubt see a downturn in their substantial private fees if they were to objectively assess whether someone was truly suffering from an injury or not. And finally we are unfortunately in times where many people are experiencing financial difficulties and so with the most minor of incidents the opportunity of obtaining £1000s for a simple, no questions asked routine of making a claim, with little or virtually no risk of ever getting found out, will no doubt present itself as too good an opportunity to miss out on.”

Anon

“Andy mentions banning referral fees is a red herring, but doesn’t go on to explain why.”

Anon

“How can industry bodies apply pressure to the government to see some ‘real action’ as David describes, to see proposed solutions forced into action?”

Anon

“Is anyone doing anything to develop proper diagnostic tests to determine whiplash?”

David Matthews

“Anyone who denies that there is a compensation culture is either in severe denial or they are earning huge amounts of money from it.”

Anon

“Of course there is. The selfish, greedy culture of taking as much as possible despite the long term consequences to everyone and the planet is unfortunately manifesting itself in all walks of life. CMC’s are the worst escalators of claims, masquerading behind the so called inability of the public to file a simple insurance claim. In a recent simple knock for knock, we were sent a detailed compensation form describing how to claim for whiplash, hire car etc. when all that was required was a wing mirror. Disgraceful!”.

Anon

“I think the CMCs are already looking for other furrows to plough – rumour has it that many have gone into overdrive to get as many claims through the door as possible before the legal aid act comes in and ruins their party. Compensation culture is alive and well, sadly.”

Anon

“CMCs get a bad rap, but the reality is that the bad apples are spoiling the proverbial barrel. Most are honest firms providing a service to busy claimants that would not otherwise have the time or know-how to make a claim themselves. Again, most are also completely transparent about their commissions. CMCs have been the scapegoat of the rest of the insurance industry for too long. ”

Anon

“I think there is a compensation culture, the question for me though, is who is to blame? I blame the lot. The insurers, the brokers, the claims management companies and the lawyers. Everyone’s in it. It’s one gigantic feeding frenzy.”

Peter Latham, Essex

“I’m not sure why anyone would think there isn’t a compensation culture. Certainly in personal injury its exploded in the last five to ten years. It’s good at least that we’re having debates like this. Shows that people are thinking about it and looking for solutions..”

Part of the Insurance and Risk group of Newsquest Specialist Media

Published by Newsquest Media Group Limited,

registered in England & Wales with number 01676637

at The Echo Building, 18 Albert Road, Bournemouth,

England, BH1 1BZ - a Gannett company

registered in England & Wales with number 01676637

at The Echo Building, 18 Albert Road, Bournemouth,

England, BH1 1BZ - a Gannett company

Site powered by Webvision Cloud