With one-third of customers giving up on lengthy question sets, will insurtech powered zero-questions-asked insurance quotes revolutionise the process?

One main differentiator of insurtech managing general agents and insurers such as Trõv, Lemonade, Lenny, Wrisk, Simplesurance, Coverly and Uinsure is the promise to provide a real-time quote without the need to answer long questionnaires.

“It’s really about getting data from lots of different sources instantaneously,” said Chris Butcher, chief executive, intermediary services at Davies Group.

“From the moment the customer interacts by tapping their phone, the app can draw down through all those data feeds almost a complete picture of the customer without them doing anything.”

Quotes without questions

Self-proclaimed insurance disruptor Uinsure has launched a home insurance product where real-time quotes are generated without the need for the customer to answer any questions.

Hailed by the insurtech firm as the industry’s “Uber/Netflix moment”, it uses information already provided to mortgage lenders to deliver binding quotes via the company’s new open application programming interface (API).

Data-as-a-service provider WhenFresh partnered with Uinsure to provide the product. It is also working with other carriers “who want to unshackle themselves from price comparison churn engines”, said WhenFresh co-founder and director Mark Cunningham.

“With Uinsure, as they are already asking for data for the mortgage, the only thing they need to ask is the additional buildings information,” he said. “And they call out to us by API, so there is zero questions asked of the applicant. The Uinsure team just deliver a price.”

Data-homogenous

WhenFresh brings together over two billion data items from various sources for nearly all residential UK properties, including the date a property was built, number of bedrooms/bathrooms, and property type and style. Available via a single API integration, insurers can extract the data they find most useful.

This is not always the data that has been traditionally requested by home insurance underwriters and brokers, said Cunningham. “Insurance is not a data-rich business, it’s a data-homogenous business. A lot of companies have the same information, but not necessarily the information you need.”

“If you knew how proximate an address was to a petrol station, how high a property was up a hill, or that there was a power line that was going to be built across a property in six months time, what would you do with it? These are the things that are going to make a difference – not necessarily how many bedrooms or how many bathrooms a property has.”

Some incumbent insurance providers are also teaming up with insurtechs to simplify the quotation process. Legal & General’s SmartQuote and Aviva’s “Get a Quote, Not a Quiz” campaign are two examples.

Aviva uses Land Registry data to simplify its quotation process, with digital director Owen Morris saying the carrier is “determined to make endless, unnecessary insurance questions a thing of the past”.

Matching up the data

But other carriers are struggling to extract value from new data sources, said Davies Group’s Butcher.

“Much as insurance is a data-rich industry, there’s probably an issue with old language around old datasets and new language around a completely different approach,” he said.

“How that’s married up over the next two to three years will be a significant challenge because there will be an expectation in the old world that data is presented to them in the format and structure that they want. It’s understanding if there are insurers out there that are genuinely entertaining a different type of data,” he continued.

“Are they willing to take a risk that the newer datasets are more interesting and useful than the older ones? Time will tell.”

“Whether zero questions or limited questions, insurtechs are trying to make the insurance quoting process as simple and transparent as possible for the broker, so customers can receive a fast and accurate end quote.

“It will be seen over the next couple of years in the loss ratios of the products if the new data sets provided demonstrable value,” added Zach Powell, managing director, AXIS Digital Ventures

Digital natives are shunning long questionnaires

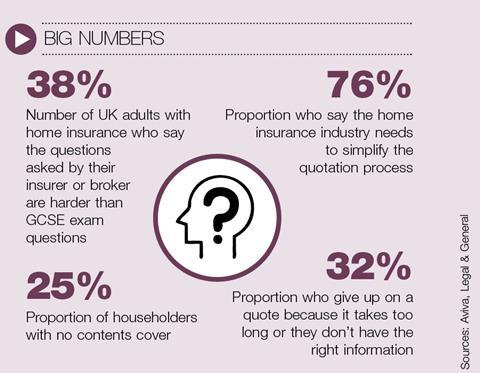

Research carried out by the Aviva found that one-third of UK adults had given up on getting a quote because it took too long to fill out the question sets, or because they did not have the right information to hand.

Three-quarters of those surveyed said insurers needed to do more to make it quicker, simpler and cheaper to take out the right insurance policies.

“Until now, taking out insurance has meant running a gauntlet of complex questions to achieve the peace of mind that home insurance can bring but many of these questions – such as the type of door and window locks – can be difficult to answer,” said Aviva digital director Owen Morris.

“By removing these difficult questions, we’re not only saving customers time, we’re reducing any worry they may have about providing the right answers.”

“We’re now able to pinpoint the risk of each property in a different way, speeding up the home application process and killing complexity.”

In March, Legal & General rolled out its SmartQuote system to intermediaries. It promises brokers will be able to get a quote for their clients’ buildings and contents insurance in as little as one question, if they already know their customer.

“[Zero-questions-asked quotations] are great for a broker. It’s taking work off their to-do list to get the deal closed,” said WhenFresh co-founder and director Mark Cunningham. “I would be surprised if brokers are not integrating with this faster than insurers.”

“For a broker, where you’re talking about a more tailored, specialised service, it is good to be able to know the information you need to make a decision between one insurance policy and another insurance policy on the basis of what the customer has told them face-to-face. You know which one to push them towards because that’s the right one for them.”

Hosted by comedian and actor Tom Allen, 34 Gold, 23 Silver and 22 Bronze awards were handed out across an amazing 34 categories recognising brilliance and innovation right across the breadth of UK general insurance.

No comments yet