Global Reinsurance editor David Sandham looks at the latest reinsurance stories making the headlines

One of this year’s most interesting reinsurance stories was a three-way tug of love between Validus, Max Capital and IPC. The otherwise gentlemanly Bermudan reinsurance market was shaken up by an agreed merger being successfully disrupted by a hostile bid.

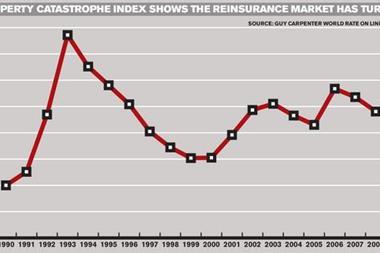

Meanwhile, further confirmation of the hardening reinsurance market came with the renewals on 1 June and 1 July. Property catastrophe reinsurance rates were up in the range of 10 – 15%, which contrasts with a 15% decline a year ago. The 1 June renewals were focussed in Florida, where although the state fund is in a better position than last year, there are still concerns about whether Florida would be able to find enough money if there was a major natural catastrophe.

A Fight to the Death

On 1 March, a merger, which had been months in the making, was announced between two Bermudan companies – Max Capital and IPC.

The deal required only the approval of the regulators and stockholders from both companies, with the former being a certainty.

A transition team was established, and Max looked set to emerge as a $3bn player.

However one month later, out of the blue, a third Bermudan reinsurer – Validus – came to the table with what it considered a superior offer for IPC.

The offer stunned the Bermuda reinsurance market: there had not been an ugly insurance skirmish in Bermuda since ACE entered XL Capital’s acquisition of Nac Re almost 10 years ago, forcing XL to pay a great deal more than its originally agreed price.

Bermuda companies speak of “friendly competition”, but the tone of Validus and Max’s exchanges became anything but friendly. Although privately, executives at both companies denied the existence of any bad blood, the merger quickly became a fight to the death.

Validus went to court to seek an injunction and argued that the $50m termination fee in the deal between IPC and Max was excessive, and that agreeing to it and to a “no-talk” provision was a breach of the directors’ fiduciary duties. In May, the Supreme Court of Bermuda denied Validus’ application for an expedited hearing for a legal suit against Max and IPC. Despite the legal position, on 18 May Validus’ sweetened its offer for IPC with a cash component of $3 per share

As the days counted down to IPC’s shareholder vote on the Max deal, the smart money was on acceptance of the Max offer. Shares in IPC are mainly held by about 200 institutional investors. Validus hit the phones to convince them its deal was the best.

Great surprise

To almost everyone’s surprise, 72% of IPC’s shareholders rejected the Max deal when the votes were counted on 12 June. Although IPC chairman Kenneth Hammond had said that a vote against Max was not automatically a vote for Validus, the disintegration of the Max combination has left IPC highly vulnerable.

If Validus does finally snag IPC, it may end up paying something less than book value for IPC’s business. Among the costs is a $50m payment to Max, written into its arrangement with IPC, should its deal fall apart, as now it has. IPC asked Validus for something nearer to its book value, but it was in no position to barter.

Will anyone else now come forward to bid for IPC? At the time of writing, with no one on the horizon, Validus looks likely to swallow up IPC before autumn sets in. That would make Validus a $3bn player, assuming that IPC’s shareholders go along this time and it seems likely that they would.

Bermuda market consolidation

So what does this say about the prospects for further consolidation in the Bermuda market?

Consolidation is supposedly overdue for the “Class of 2001” – the reinsurers which set up in that year. Its predecessor, the companies formed in Bermuda in 1993, had been reduced to just a hind end (including IPC) within five years, although a continuing soft market was a major factor. In the mixed markets that have prevailed since 2001, the comparison is a little odious.

Some say that to be taken seriously these days, a reinsurance company needs $1.5bn or $2bn in capital. Solely on that basis, there are a few merger candidates that readily present themselves —Hiscox, Montpelier Re Holdings, Max itself, Lancashire Holdings and Flagstone Reinsurance Holdings have capital of less than $1.5 bn, while Platinum Underwriters Holdings has less than $2bn.

Given the continuing rarity of credit, any acquisitions would have to be funded by shares, as in the main is Validus’s offer for IPC, and as would have been Max’s deal.

While the shape of future deals is unclear, one lesson is clear. Directors must at all times consult closely with their shareholders and fight hard to create value for them.

Hurricane shortfall

Last year, no major storms made landfall in Florida, leaving insurers and reinsurers alike breathing a sigh of relief. Not least because the state of Florida faced huge deficits in its catastrophe fund should a major storm have hit, thanks to the economic crisis. At the end of last year, the Florida Hurricane Catastrophe Fund estimated it would have had a $14.5bn shortfall if a hurricane had hit, thanks to the unprecedented municipal bond market conditions in the middle of the global credit crisis. Now, the fund is in a far better position with some major legislative changes, one of which was signed into law on 27 May, having helped it.

However there are still concerns around whether Florida would be able to find enough money in case of a major natural catastrophe. As the 2009 hurricane season progresses, insurers and reinsurers will again be watching the storms stacking up in the Atlantic Ocean like so many aircraft waiting to land. And – if a hurricane looks like it could make landfall in Florida – they will again be holding their breath.

P & C reinsurance hardens by 15%

The 15% increase in property catastrophe (P&C) reinsurance rates on 1 June 2009 set the tone for a 10% – 15% increase at the 1 July renewal. The 1 June renewal is a “bellwether” and often influences future trends, according to Chris Klein, global head of business intelligence at Guy Carpenter.

Both of the renewal dates are important. 1 June is focussed on Florida, a significant and substantial peak-risk zone. There is also a strong political dimension to 1 June renewal, given the importance of the state government in the provision of hurricane cover. Reinsurers must reserve capacity for 1 June, and look carefully at what they write to ensure they maintain their books in a balanced way in terms of territories and perils.

Klein described the market in Florida as “finely balanced” with the range of quotes described as “narrow”. On average firm order terms came in at 95% of the standard quote. The narrow spread between quotes and bound treaties showed that reinsurers were “not having to give away much”.

The 1 June P&C increase compares to a 15% decline a year ago.

But it is a broader renewals season on 1 July. In the US many classes were renewed, across local regional and nationwide programmes. Other parts of world also had renewals on 1 July, including Latin America, the Caribbean, Mexico, and Australia.

“With four major renewal periods having been completed in this calendar year, there is a general sense of calm the reinsurance markets,” said Klein.

No comments yet