Insurance DataLab reveals the preliminary findings of its 2022 Broker Performance Report exclusively in Insurance Times, rating the performance of different sized brokers based on their financial performance

The Covid-19 pandemic has had a profound effect on the entire UK insurance industry - and the broking market is no exception.

Despite the myriad challenges presented by the pandemic, broker M&A has continued unabated in recent years. Research from advisory firm Imas, published in February 2022, revealed that 2021 was a record year regarding the volume of M&A deals, thanks to 145 transactions that totalled more than £6bn.

This means that growth at the top end of the broker market has increased over the last 12 months, as evidenced by the reported levels of revenue that are controlled by the UK’s leading brokers.

Analysis from Insurance DataLab’s inaugural Broker Performance Report, published exclusively by Insurance Times this month, has ranked 132 broking firms on their performance across three key metrics – profitability, productivity and growth.

For the purposes of this analysis, the broker market is defined as the 132 brokers evaluated by Insurance DataLab.

The five largest firms – all of which reported revenues greater than £500m for 2020/21 – account for around 49% of the pool of 132 brokers, with a collective revenue of almost £4.6bn, according to the firms’ latest financial reports.

This is an increase of more than £340m compared to Insurance DataLab’s 2021 figures, based on 2019/20 comapny accounts – when these five brokers accounted for 46% of the market and had an overall revenue totalling around £4.2bn – as well as more than £600 higher than the previous year, when these five brokers accounted for 45% of the market.

Indeed, over this three-year reporting period, market share for the brokers that reported revenue between £100m and £500m in 2022 has remained steady at 31%, while the market share for brokers reporting revenue between £10m and £100m for 2022 has fallen four percentage points to 17%.

Meanwhile, the smallest brokers in this analysis – with revenues of less than £10m in 2022 – accounted for 3% of the market in 2020, compared to just 2% this year.

Largest brokers on top after marked improvement

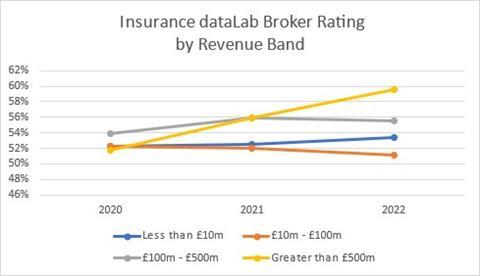

Continued growth from the brokers at the top end of the market has added fuel to their performance over the last 12 months, with brokers earning more than £500m rising to the top of Insurance DataLab’s rankings and recording an average broker rating of 57.9% for 2022.

This represents a two percentage point improvement on the 55.9% rating the five largest brokers received in 2021 and is also 4.7 percentage points higher than the 53.2% rating received in 2020.

This improvement means that 2022 is the first year within the last three years where the largest brokers in the UK have reported the best average performance in the market, after finishing second in both 2021 and 2020.

Brokers boasting more than £500m in revenue replaced their smaller peers at the top of Insurance DataLab’s rankings after brokers with revenue between £100m and £500m received an average rating of 55.5% for 2022, the second highest in this analysis.

This latest performance is 0.4 percentage points lower than the 55.9% rating this demographic received for 2021, however 2022’s rating remains 1.6 percentage points higher than the 53.9% rating this group received for 2020, when they were ranked top in Insurance DataLab’s broker performance ratings.

The third highest rated group of brokers for 2022 featured businesses that reported a revenue of less than £10m, with an average broker rating of 53.4%.

This marks a 0.9 percentage point improvement on the 52.5% rating this category received for 2021, when these smaller brokers finished yet again in third spot, and is 1.1 percentage points higher than 2020, when they received a rating of 52.3%.

Finishing bottom of Insurance DataLab’s rankings for 2022 are brokers that reported a revenue between £10m and £100m – this demographic picked up an average broker rating of 51.1% this year, the lowest of any broking group across the full three years of this analysis.

This means that this broking category has reported a declining rating in each of the last two years after receiving ratings of 52% and 52.3% in 2021 and 2020 respectively.

In fact this means that these mid-sized brokers have now finished bottom of Insurance DataLab’s rankings across all three years of this analysis, with the gap to those above them widening each year.

Continued growth adds fuel to fire for largest brokers

Brokers included in this analysis with revenue in excess of £500m have performed the best under Insurance DataLab’s growth metric, recording a 2022 average growth rating of 58.2% and outscoring all other broker groups by more than seven percentage points.

Indeed, while the growth rating for the other broker groups fell over the course of this analysis, brokers earning more than £500m have increased their average score, rising from 57.1% in 2020 and after peaking at 59.1% in 2021.

The second highest rated group for growth over the last year goes to brokers that reported a revenue between £100m and £500m – these firms have a growth rating of 51.1%, which is in line with the overall market average.

This was, however, still lower than the 54.6% average growth rating this group received in 2021 and also worse than the 52.4% rating it received for 2020.

Brokers with revenue between £10m and £100m, meanwhile, have experienced the largest decline in their growth rating over the last three years, with the average score for this group falling from 54% in 2020, to 52.5% in 2021 and 50.6% in 2022.

This means that brokers with revenue between £10m and £100m have fallen from being the second highest rated group of brokers for growth in 2020 to the lowest ranked group in 2022.

The final group in this analysis – brokers that reported a revenue of less than £10m in 2022 – remained relatively steady in their performance under Insurance DataLab’s growth metric.

This group picked up an average score of 50.7% for 2022, compared to ratings of 51.1% in 2021 and 51.4% in 2020.

Despite this steady performance, this category still performed worse than the market average across each year of this analysis.

Mid-sized brokers make most of scale to boost efficiency gains

When it comes to productivity, brokers with revenue between £100m and £500m were the highest performing broking group, picking up an average productivity rating of 58.3% for 2022.

This is a marked improvement on the 54.9% average rating the group received in 2020 and is also better than the 57.3% rating it received for 2021.

This strong performance was driven by particularly low staff costs as a percentage of turnover, with the group picking up an average standardised score under this measure of 72.9% for 2022.

Turnover per employee, however, was not as impressive, with this broker category picking up a standardised score of just 43.7% for this metric.

The second highest rated group for productivity was brokers with revenue in excess of £500m. This group picked up an average rating of 53.6% for 2022 – up from 52.5% in 2021 and 49.9% in 2019, when it was the second lowest ranked group in this analysis.

Meanwhile, brokers with revenue between £10m and £100m received an average Insurance DataLab productivity rating of 52.5% in 2022 - down from 54.4% in 2021 and 53.1% in 2020.

And, in another sign demonstrating the benefits of scale when it comes to efficiencies, brokers with revenue of less than £10m were the lowest ranked group in this analysis for productivity, picking up a rating of 49.4% for 2022.

This was, however, still an improvement on the 48.7% rating this demographic received for this measure in 2021, as well as better than 2020’s rating of 47.9%.

Biggest firms benefit from profitability boost

When it comes to profitability, it was the big players that once again came out on top. Brokers with revenue in excess of £500m received an average profitability rating of 59.8% for 2022 - up from 54.4% in 2021 and 50.8% in 2020.

This performance came as a result of the five largest brokers in this analysis reporting an average three-year earnings before interest, taxes, depreciation and amortisation (Ebitda) margin of 25% in 2022, some four percentage points higher than the market average.

Meanwhile, brokers with revenue between £100m and £500m were ranked second under Insurance DataLab’s profitability measure, with an average 2022 rating of 58.6% - up from 56.6% in 2021 and 54.9% in 2020.

The smallest brokers in Insurance DataLab’s analysis are next in terms of profitability, punching above their weight with an average profitability rating of 58.2% for 2022.

This is a 2.4 percentage point improvement on the 55.8% average profitability rating this category received for 2021 and a 2.8 percentage point improvement on its 55.4% rating for 2020. This group of brokers with less than £10m of revenue outperformed the market average across each year of this analysis too.

Finally, the lowest ranked group of brokers for profitability was those that reported revenue of between £10m and £100m. This demographic attained an average profitability rating of 51% for 2022, compared to 50.2% for 2021 and 50.1% for 2020.

This means that this group have failed to achieve an average profitability rating higher than the market average in any of three years of this analysis.

Methodology

The performance metrics used for this research have been calculated using Insurance DataLab’s own analysis of insurers’ company accounts filed at Companies House, which takes into account both short and long-term performance over the last three years of trading.

The three metrics used to calculate the overall Insurance DataLab broker rating are:

- Profitability: Insurance DataLab calculated the three-year aggregate earnings before interest, tax, depreciation and amortisation (Ebitda) margin by dividing the aggregate Ebitda figure by the aggregate revenue generated over the last three years.

- Growth: Insurance DataLab calculated a growth metric comprised of a weighted average of the growth in revenue over the last 12 months and the growth in operating profit over the same period.

- Productivity: Productivity has been assessed by looking at staff costs as a percentage of turnover over the last 12 months, as well as the turnover generated per employee over the same period.

Each metric has subsequently been standardised to create a percentage score for each broker, with a weighted average used to create Insurance DataLab’s overall rating.

Full details of how these metrics have been calculated, as well detailed performance ratings for the 100 largest brokers, are available in Insurance DataLab’s Broker Performance Report.

No comments yet